Most people automatically get their Part B as the same time as their Part A; they’re excited to be saving money by going on Medicare and are ready to go!

But sometimes it makes sense to only apply for Part A or even to give back Part B if you’ve been automatically enrolled. You are not required to be keep Part B! Here are a couple of examples:

You’re turning 65 but you or your spouse still work and have great coverage through work – just apply for Part A, especially if you’ve already worked your 10 years/40 quarters. 1) It doesn’t cost you anything; 2) you can determine your own Special Enrollment Period for Part B when you need it.

You’ve had more than 24 months of Social Security Disability and Social Security sends you a Medicare card with both Parts A and B – this depends upon your own situation. If your employer and/or spouse’s group coverage meets your needs, they let you stay on it, and the creditable group coverage costs less than paying for the Part B premium, a Medicare Supplement, and a prescription drug plan, then ride your employer’s pony until you hit age 65! Click here to download the CNS-1763 “Disenrollment from Part B” form so you’re not stuck paying for premiums you won’t be using. (You have to download the form from that page.)

You can always apply for Part B later (yes, the form is available for that, too!) But consider: If it costs more to go with employer coverage, depending on your situation, it may make more sense to just pay your Part B premium and go with a $0 premium Medicare Advantage plan. There is no “one size fits all” in Medicare, so talk to me to see if you would do better on Medicare with Part B or not. I will help with the math!

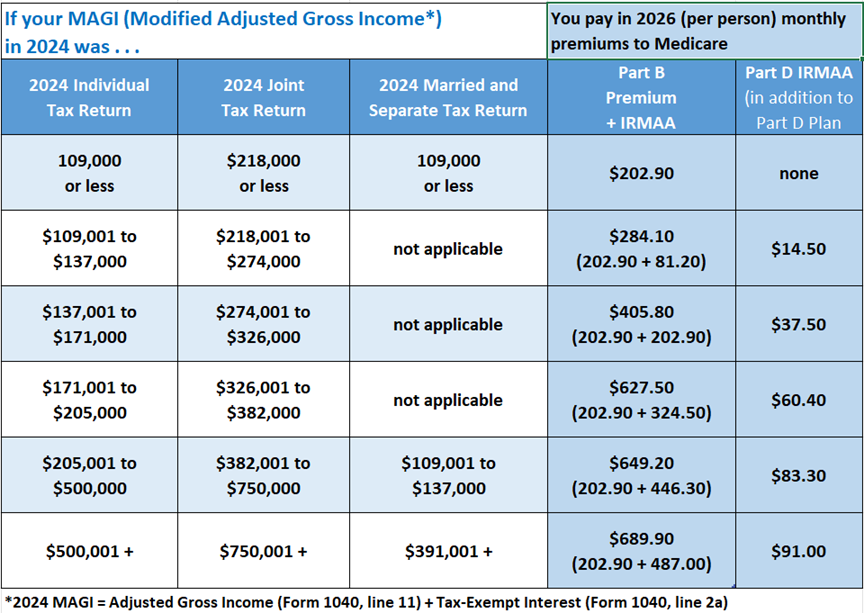

What if I’m Not the Average (Financial) Bear?

Those earning higher incomes will pay the standard premium plus the Income-Related Monthly Adjustment Amount (IRMAA). IRMAA is an extra charge added to your premium. (Notice the actual cost of Part B? It’s $698.80! The Feds subsidize your premium.)

But That’s Not Fair! I Don’t Make That Much Anymore!

If you had a “life-changing event” in 2024, the Feds don’t know that it was a one-time anomaly. What do they consider “life-changing”? Marriage, divorce or annulment, death of your spouse, work stoppage or reduction, loss of income-producing property or pension income, or employer settlement payment. (They changed the reasons for the exemption in December 2022 while we weren’t looking!) Click here for form SSA-44 to avoid paying a surcharge! (Make sure you call me before Medicare talks you into paying three months’ worth of Part B premiums while you’re disputing the IRMAA – you ARE allowed to only pay them for one month!)

I Need to Apply for Medicare Part B Right Now!

If you already have Part A, then click here for the form. (Talk to me first to see what date you should request in the Remarks section of the form.)

Okay – and if you’re just now applying for Part B AND you’ve had creditable coverage, they’ll want you to prove it. Click here for form CMS-L564 to prove you’ve had prescription drug insurance all along. All you have to do is fill in Section A, then your HR department can do the rest. (I recommend you have HR do their magic first, then you can copy the dates they will put on their form into your Part B application. Less wear and tear on you!) Make sure to write when you want Part B to start in Section 9, Remarks, or they could just start you next month when you actually wanted to start sometime later! When both of your forms are ready, drop them off at your local Social Security office.

You may apply online for Part B as well, even if you’re not leaving employer group coverage. The online version will ask you to upload some forms, so give them your current Medicare card with the Part A on it and then a copy of your current insurance card!

Umm, I never applied for any Medicare when I had the chance . . . can I get it now?

If you’ve let your Medicare Birthday pass without applying for any Medicare, you can apply between January 1st through March 31st of the year (this is the General Enrollment Period). Your Medicare coverage will start the following month.

If you’re over 65 and have never applied for Part A or B, and you’ve missed the General Enrollment Period, perhaps you had an Exceptional Condition? Read about it on the How to Apply for Medicare page.

Have you had a health insurance plan with creditable drug coverage? Then at least you won’t be hit by any kind of Part A, B, or D late enrollment penalties. (More on the late enrollment penalties in the in the Don’t Be Late! page – click here to jump there now.)

Required Disclaimer: “We do not offer every plan available in your area. Currently we represent 0 to 28 organizations that offer 0 to 28 or more products in your area. Please contact Medicare.gov, 1-800-MEDICARE, or your local State Health Insurance Program to get information on all of your options.” So there.