Make sure you’re covered for those days when you wake up on the wrong side of the bed!

How do you like to access medical care? You have a choice! Below are the different ways health plans give access to their providers.

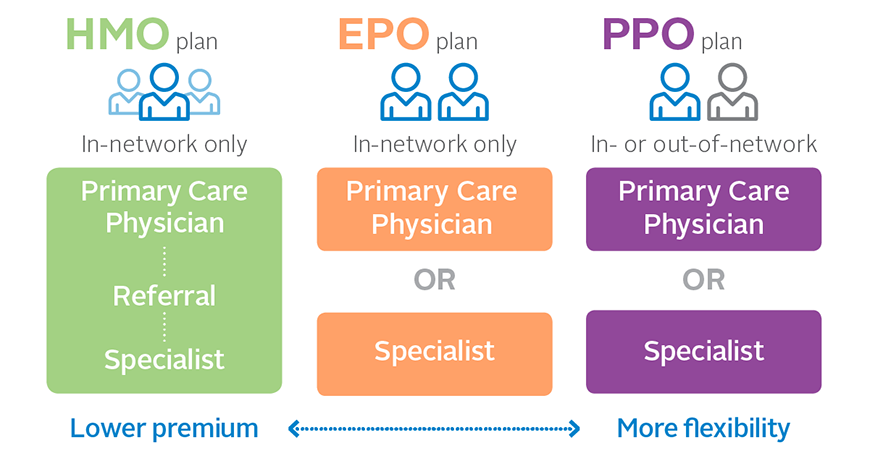

HMO:

Health Maintenance Organization – you select a primary care physician (PCP), who authorizes treatment with specialists. This is generally the most cost-effective option. You must receive all treatment through one medical group or Independent Physicians Association.

PPO:

Preferred Provider Organization – you can self-refer to any physician, though you will probably pay more for doctors not in your insurance company’s network. You are free to see physicians from various medical groups.

EPO:

Exclusive Provider Organization – priced like an HMO but you self-refer like a PPO. You need to see physicians who are contracted with the insurance company’s network, though not specifically a medical group.

A Little Health Insurance Lingo Here

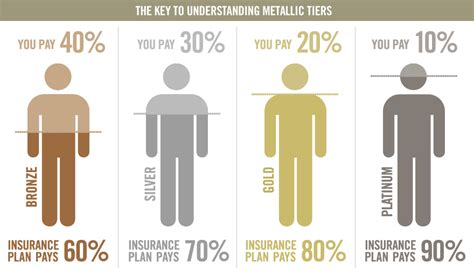

The Metal Tiers: Each health insurance plan metal tier – Bronze 60, Silver 70, Gold 80, or Platinum 90 – is required to have the same exact deductibles, copayments, etc. below for that tier. So if you’re seeing some of the companies have higher premiums than others, you are paying for access to more physicians and/or specific hospitals that are not contracted with every company.

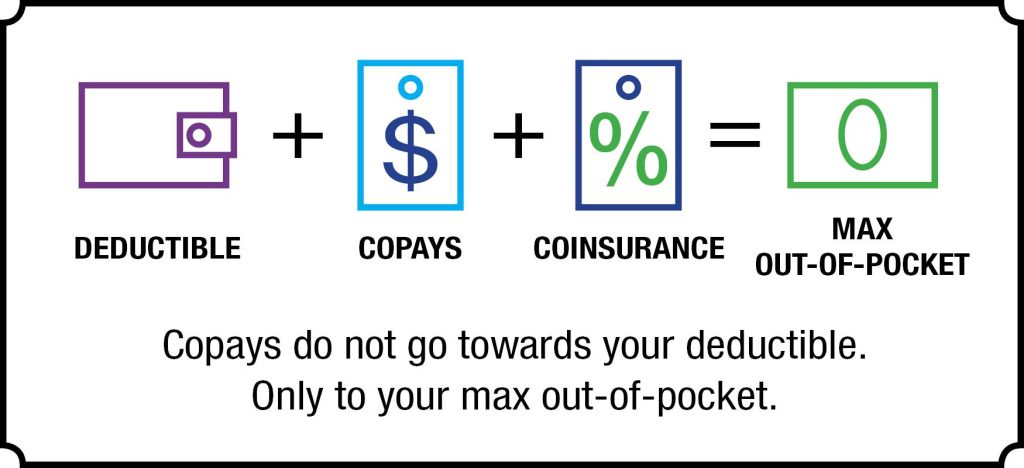

Premium: How much you pay every month to be enrolled in the plan.

Deductible: The amount you pay before the insurance company pays their part for a service.

Copayment: The amount you pay to the doctor or physical therapist, etc. when seeking care. Most of your costs on a health insurance plan will be as copayments.

Coinsurance: A percentage you pay with the health plan for a covered service. You may see a coinsurance to buy durable medical equipment (DME) like canes or walkers. You pay a percentage of the total cost for that equipment instead of a copay.

Annual Out-of-Pocket Maximum (the Stopgap): This is the most you would pay for covered services in a calendar year. After you spend this dollar amount on deductibles, copayments, and coinsurance for in-network care and services, your health plan pays 100% of the costs of covered benefits for the rest of that calendar year. This is one of the biggest advantages of having health insurance – there is a limit to the amount of money you could be liable for in a year.

Reminder: Like water in a channel, as part of an HMO health insurance plan, you must stay in your lane, or in your case, your medical group or network. You choose a medical group and receive services from doctors and hospitals in that group. If you have a PPO, you can go to doctors in or out of your network, and you don’t have to stay with any one medical group.

Medical Groups vs. Networks

If you choose an HMO plan, then underneath your health insurance plan is your medical group – the insurance company provides the financial protection and the medical group provides the actual medical treatment.

Which medical group you choose makes a difference! Did you know that certain hospitals only take patients from specific medical groups for scheduled procedures? Example: If an ambulance takes you to Humungous Hospital in an emergency, you’ll be treated because it’s an emergency, but if you want a knee replacement at that hospital, you need to belong to one of their selected medical groups to have access to their hospital for your surgery. Even if your plan is accepted by that hospital, if your medical group doesn’t, you don’t get to pick that place. So both insurance plan and medical group need to align to access the hospital of your choice. This is where it’s helpful to have a broker (like me!) to help you, because I know which groups go to which hospitals!

If you select a PPO plan, then rather than having to stay within one medical group, you choose from your health insurance company’s network of providers. You can go “outside of network” or see someone not contracted with them, but you would have to pay out of pocket until your deductible is reached, then you would have a reimbursement of 50% or whatever is the contracted rate with your company. In the case of PPOs and hospital access, similar to the HMOs above, your plan has to be contracted with your hospital of choice if you wish to receive services there.

On- vs. Off-Exchange Plans

On-Exchange (With Subsidy):

Do you qualify for a government subsidy? A subsidy is a credit towards your health insurance premium that the federal and often state government offer to people under certain income amounts. To get a subsidy in California, you would have to have insurance on the Covered California exchange. The discount can vary by ZIP code and number of people in your “household” (basically, the number of people who are present and accounted for on your tax return!). There are lots of questions you must answer when we’re working on your subsidized application.

Another thing about On-Exchange plans is that you can enroll up until the day before coverage is effective, so for a plan ready to use next month, you can enroll by the last day of THIS month. They don’t do that with the Off-Exchange plans.

The American Rescue Plan

If you’re on a Covered California Silver 70 plan, you fall under the recent American Rescue Plan legislation. In August 2022, Congress extended the ARP through 2025 so you can having savings for a while! This mostly affects people with HMO and EPO coverage, but there have been some savings for those of us on PPO plans also. Want to see how much you could pay? Give me a call at (714) 657-6355 with the information in Ready to Start? below.

People with Employer-Sponsored Coverage

Is your company’s health insurance really expensive? If your company’s lowest-cost health plan is 9.02% or more of your household income, you may qualify for a subsidy! I can run an estimate on savings, but I’ll need to know how much just the employee’s cost of insurance is, then also the cost for the entire family, against their total income. If the calculation falls in their favor, they can get the federal subsidy.

Off-Exchange (Without Subsidy):

If your income is higher, or on the edge, I then check with the companies in your area to see if it’s more cost-effective to go directly with them “off exchange.” I can save you hundreds of dollars a year by checking this way – and by going direct, there are lot of less questions and requirements!

Want to be effective by next month? Then you must enroll by or before the 15th of the current month to start off-exchange coverage on the 1st of the next month. Don’t shoot the messenger!

A Word about the California Health Insurance PENALTY

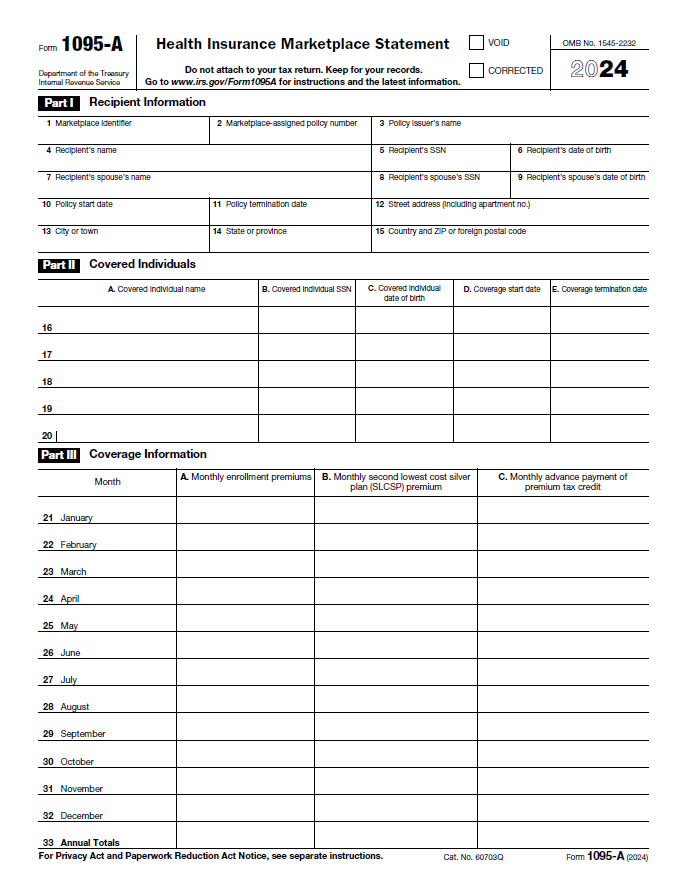

This is important, so pay attention: When the Feds removed the Obamacare penalty for not having health insurance, California Governor Newsom said, “Another tax? What a GOOD idea!” So if you don’t have health insurance, you may be fined a minimum of $900 per adult and $450 per child on your state income taxes! There may be exceptions though, so click here to learn more. To avoid this penalty, make sure to file your 1095-A.

Ready to start? Before you call me, please send me the following:

- Your ZIP code

- Your estimated household income for this year, and

- The ages of all the people in your household/on your income tax form (whether they’ll be insured or not!)

- For a more tailored quote, please tell me if you have any special doctors you absolutely need or medical groups or hospitals you prefer.

With the above information, I can return a fast quote to you by email or text.

Do you live in a state other than California? I can help!

To check out the plans in other states, click here. You’ll be able to see all the plans and enroll yourself. If you’d like me to help, give me a call.

Do you need insurance but would like to do it yourself? Most California hospitals take Blue Shield PPO plans, and many take the Blue Shield Trio HMO too! Click here to enroll in a Blue Shield Individual and Family plan – Medical, dental, and/or vision!

Health Net also offers direct PPO and HMO plans. You can check them Health Net plans here.

Take a look at Anthem Blue Cross for great plans in your area as well as dental and vision plans from Anthem here.