Medicare Part D

What Is It, What Does It Cover and Not Cover?

Medicare Part D is medication insurance, a federal program administered by private insurance companies. It helps cover brand-name, generic, and specialty medications. It started in 2006, and before that, thousands of Medicare beneficiaries had a hard time with retail drug costs. Like Part B, it also has a yearly deductible; in 2026 it’s $615.

When Am I Eligible for Part D?

You are eligible for Part D when you are enrolled in either Part A and/or Part B. You must live in the plan’s service area.

How Do You Get Part D?

You can enroll in Part D prescription drug plan (PDP) or enroll in a Medicare Advantage plan with drug coverage, such as a Part C Medicare Advantage Prescription Drug (MAPD) plan. If you choose a PDP, then your drug insurance plan is separate from your Medicare Supplement card, if you have one.

How Does Part D Work?

If you choose an MAPD plan, your Part D and usually the deductible is included in the plan. If you choose a PDP, you pay a monthly premium to an insurance carrier for your Part D. Then, you use the insurance carrier’s network of pharmacies to buy your prescription medications. Instead of paying full price, you pay a copay or a percentage of the drug’s cost, depending on the drug’s Tier.

Formularies and Tiers

Prescription coverage varies by plan; every plan has a list of drugs that the plan covers, known as a formulary. Some plans have very broad formularies, covering many costly drugs, while others have limited formularies, so take your plan into account if you take a lot of different medications.

Drug Tiers are another important consideration when choosing a drug plan or a plan with drug coverage. Here are the levels:

Tier 1 – Preferred Generic Drugs (lowest copay)

Tier 2 – Generic Drugs (medium copay)

Tier 3 – Preferred Brand Drugs (higher copay)

Tier 4 – Non-Preferred Drugs (higher copay)

Tier 5 – Specialty Tier Drugs (highest copay)

Tier 6 – This is sometimes called the Select Tier; not all plans carry a Select Tier, and this tier often offers such medications as Viagra or weight-loss medications for a very low cost. (You won’t find this on a stand-alone Part D drug plan, only on a Medicare Advantage Prescription Drug (MAPD) plan.)

Prescriptions in Tiers 1, 2, and 3 are based on many factors, like percentage of ingredient (1% vs. 2%) and type of medication (lotion, cream, tablet, capsule, liquid, suppository, etc.). This is why I’m so specific when I talk to someone about their medications and the dosages and how the drug is delivered.

As I said before, it pays to compare drug plans, as companies some will have medications at a Tier 3 while others have that same drug at Tier 2, a big difference in cost.

The Three Stages of Medicare Part D

The Annual Deductible

In 2026 the annual Part D deductible is $615; a few Medicare Advantage Prescription Drug plans and a few expensive stand-alone prescription drug plans covered the deductible 100%, so you may go straight to Initial Coverage. Many plans will skip the deductible on Tiers 1 and 2, but will charge a partial or full deductible for Tiers 3 through 5.

Initial Coverage

During this stage of Part D drug coverage, you will pay a copay for any medications based on their tiers, above. The insurance company AND Medicare both track the spending by you and the insurance company until together you have spent a total of $2,100 this year. At this point you have reached Catastrophic Coverage, and you’re done paying for prescription medication for the rest of the year!

Which Costs Go Toward Catastrophic Coverage?

- Any deductibles you or your insurance company paid;

- The retail costs of your medication after you have met your deductible. (Note I didn’t say cost of drug copays, retail cost of a medication could be many times more than the copay!)

YIKES, The Pharmacy Wants $$$$ Right NOW! Don’t worry, use the M3P!

In 2026 you can spread out the costs of your medications. If your medications are already at $2,100 in January, then take advantage of the M3P. The M3P is the Medicare Prescription Payment Plan. You can spread out your $2,100 cost over the entire year, or however many months are left of it, by making monthly payments to your insurance company. Now you can just go pick up your medications at the pharmacy. This way the most you would pay in a month if you start in January is $175/month.

What Other Things Affect Drug Costs?

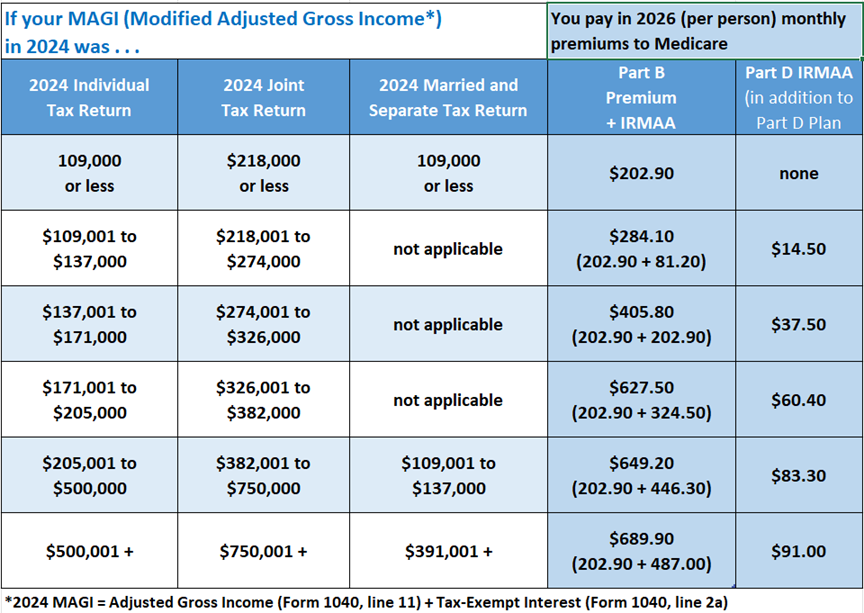

Higher Premiums for Higher Income!

Remember our friend, IRMAA? She likes to raise Part D premiums too! Here’s another look at the IRMAA chart – take a look at the last column on the right to determine your extra premium.

Late Enrollment Penalty (LEP)

If you don’t sign up for a drug plan when you first can, there is a permanent 1% per month Late Enrollment Penalty for all the time you could have had a drug plan and didn’t. So someone missing Part D for two years would pay 24% times the National Average Premium, which this year is $38.99; this would be a penalty of $9.36, rounded up to $9.40 a month in 2026!

Is that Late Enrollment Penalty “Permanent” Permanent? Yes, unless you qualify for a Low-Income Subsidy, at which point that LEP is on hold!

Don’t think you owe it? Appeal the penalty with this form.

Some Ways to Lower Drug Costs

Low-Income Supplement (LIS) – also called “Extra Help”

A Low-Income Supplement (LIS) provides help with prescription drug costs by helping with the monthly Part D premium annual deductible, and copayments. The amount of subsidy depends on your income compared to the Federal Poverty Level and resource limitations set by Social Security every year. For more about LIS and applying, click here, because “The Rent” is just too darned high.

Chronic Special Needs Plans (C-SNPs)

Do you take heart medicine or inject yourself with insulin (or both!)? There’s help for the costs of various specific medications through C-SNPs. Some Medicare Advantage companies have plans that cover medications for asthma, diabetes, heart disease, and even mental disorders with specialty plans, and part of their benefit is a reduced cost for medications for those specific conditions. For example, in California there are plans that cover certain kinds of insulin for zero! When I have a client on this kind of plan who uses insulin, I write a letter to his or her doctor listing the zero-copay insulins and request that my client have one of those prescribed. That’s one way to save money!

Use a Discount Program

If your insurance company has rather high copays on generics, look into discount programs, like GoodRX, SingleCare, or Perks.Optum. You could save a lot of money using these programs rather than going through your insurance. Please visit When the Rent is Too Darned High to read more about drug discount programs, at the end of that webpage.

Some Questions About Part D

Q: I don’t take drugs, why should I get a Part D plan?

A: See Late Enrollment Penalty, above! Avoid this problem by getting an inexpensive PDP. Depending on your state, I’ve seen them for $0 a month!

Q: How much are Part D premiums?

A: It depends on your needs. If you use little to no medications, there are some extremely low-cost plans available – and some extremely expensive ones, too!

Q: What if I have other insurance?

A: If you have continuous creditable drug coverage through Medi-Cal/Medicaid, an employer or union group, COBRA, TRICARE, TRICARE for Life, etc, you’re won’t be fined for not having a drug plan if you choose a private one later. Just make sure you have proof!

Q: What’s that “Creditable Coverage” thingie again?

A: It’s drug coverage that at least as good or better than that required by Medicare.

Required Disclaimer: “We do not offer every plan available in your area. Currently we represent 0 to 28 organizations that offer 0 to 28 or more products in your area. Please contact Medicare.gov, 1-800-MEDICARE, or your local State Health Insurance Program to get information on all of your options.” So there.